3Q25 Bank Earnings Credit Risk Deep Dive: Shifting From Stability to Specifics

Executive Summary / Key Themes

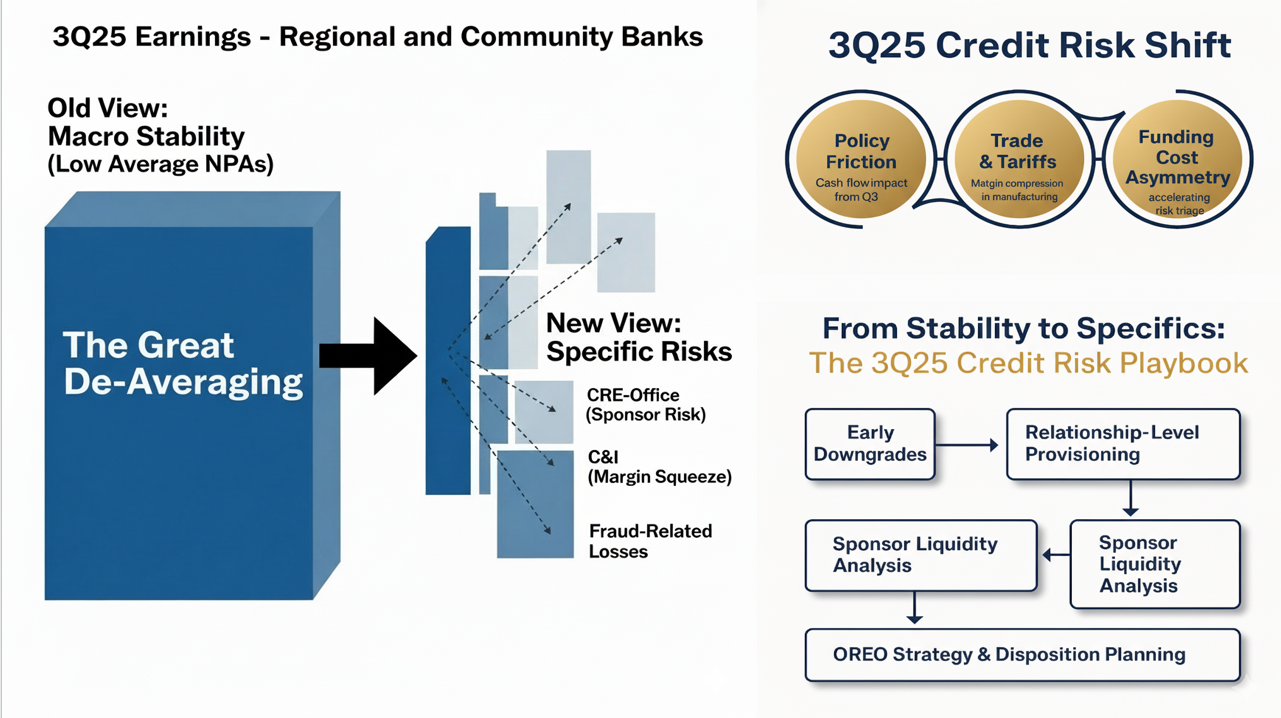

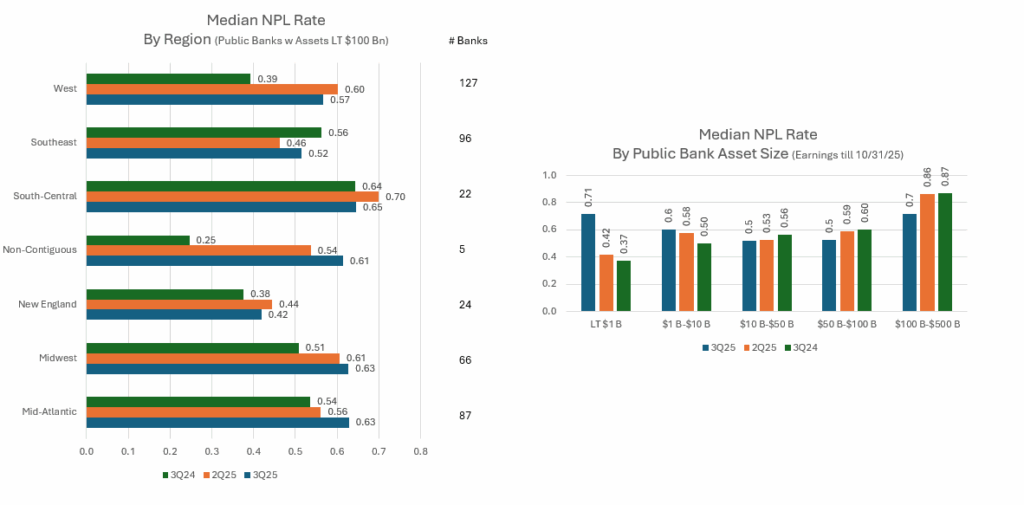

The third-quarter 2025 earnings season has confirmed the start of “The Great De-Averaging” in credit. Our analysis of bank earnings of 427 publicly listed banks with assets less than $100 Billion and earnings call commentary from 97 regional and community banks shows that portfolio-wide averages are no longer reliable indicators of risk. While headline metrics like non-performing assets (NPAs) remain broadly stable, this calm surface hides significant, diverging undercurrents.

Headline asset quality remained solid—non-performing assets (NPAs) and net charge-offs (NCOs) stayed at low levels—but beneath the surface, credit migration and portfolio segmentation accelerated.

The dominant theme is a structural shift from broad, macroeconomic-driven risk to specific, idiosyncratic credit risk, concentrated in known problem areas. The lagged effects of the “higher-for-longer” rate environment are now being amplified by three key macro overlays:

- Policy Friction: The lingering cash-flow impact of the Q3 government shutdown on specific C&I sectors.

- Trade & Tariff Impact: Persistent tariff-related margin compression in the manufacturing and logistics sectors.

- Funding Cost Asymmetry: Higher funding costs are forcing banks to be less patient with marginal credits, accelerating proactive risk management.

This environment is separating winners from losers, and the focus has definitively shifted from “if” credit will normalize to “where” the specific impairments will land.

Banks reported increasing granularity in reserve management and heightened attention to risk-rating system modernization, sponsor support in CRE, and rising OREO balances.

Section 1: Overall Commercial Credit

The overarching story in commercial credit is one of proactive normalization. Banks are no longer waiting for 90-day delinquencies to act. We observed a distinct trend of accelerated, management-driven credit migrations, moving loans from “Pass” categories directly to “Special Mention” or “Substandard-Accruing” based on forward-looking indicators, not just payment status.

Institutions like Ameris Bancorp and Umpqua Bancorp noted modest but deliberate negative credit migrations—pass-graded loans being proactively downgraded to special mention or substandard-accruing categories. This reflects the new playbook of credit management: acting early to preserve flexibility.

This proactive re-grading is a direct consequence of risk-rating system modernization. Banks like Commerce Bancshares noted they are “enhancing risk-rating systems to be more forward-looking” by integrating sponsor liquidity metrics and submarket vulnerability scores, moving beyond simple DSCR and LTV covenants. Other banks described internal overhauls of their risk-rating frameworks to incorporate forward-looking indicators of sponsor liquidity, market vacancy forecasts, and borrower stress signals.

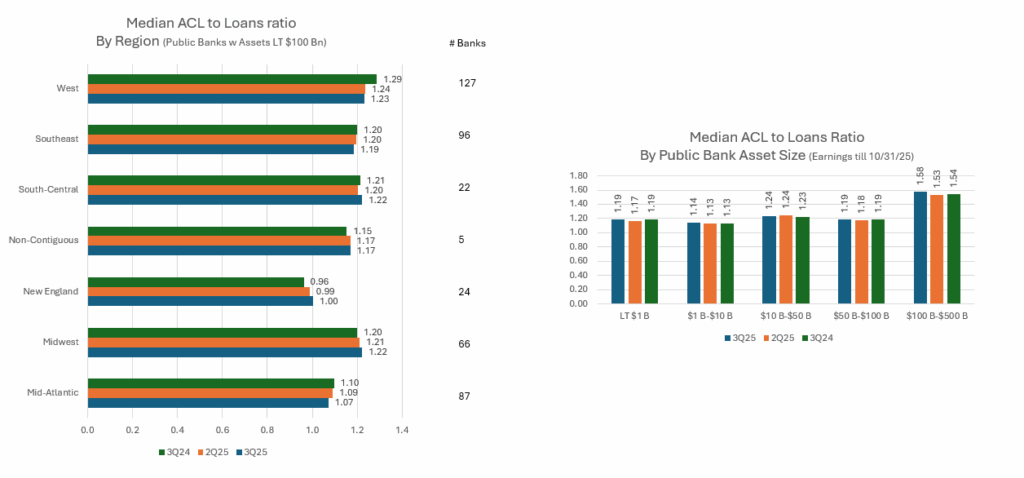

This quarter also saw a logical shift in provisioning. The era of building general CECL reserves against a worsening “reasonable and supportable” forecast is over. Provisioning is now surgical, tied directly to these specific, proactive downgrades in CRE-Office and on a case-by-case basis in C&I. Most banks maintained steady provisions, but an increasing number—such as Western Alliance Bancorporation—highlighted that PCLs were now driven by relationship-level reserves.

Illustrative Quotes:

Bank OZK highlighted its ongoing vigilance on loan performance despite strong asset quality metrics: “We continue to operate with a disciplined credit culture and maintain conservative underwriting standards across all portfolios.”

Primis Bank noted a similar stance, emphasizing that loan growth is being deliberately moderated to align with funding costs and margin preservation. “We’ve slowed loan growth intentionally—this is a balance-sheet defense year.”

Section 2: Loan Growth and Portfolio Rebalancing

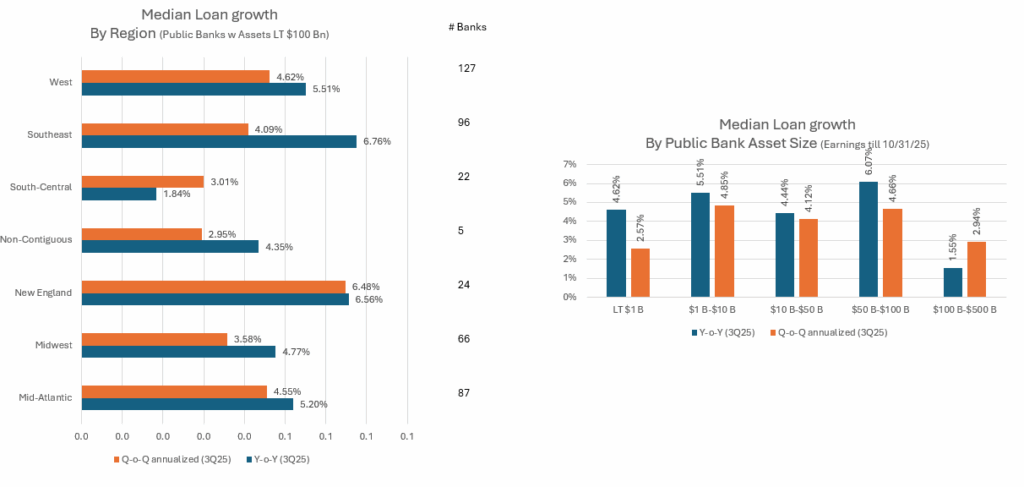

Unsurprisingly, the 2026 outlook for loan growth is muted. The commentary from 3Q25 reveals a perfect storm of slowing demand and tightening supply. On the demand side, C&I clients are postponing capital expenditures due to economic uncertainty and high borrowing costs. On the supply side, banks are responding to the environment with stricter underwriting, higher funding costs, and a clear “risk-off” posture, reserving capital for only the highest-quality, relationship-based opportunities. Additionally, Liquidity positioning is a defining constraint on loan growth. Multiple banks, including Home Bancshares, Inc. and First Internet Bancorp, reported that funding strategy—not loan demand—is the gating factor. Balance sheet optimization and “deposit defense” remain as strategic as credit discipline.

- Many institutions emphasized core relationship lending, particularly within C&I and owner-occupied CRE.

- Growth is largely being constrained by deposit funding costs, CECL capital impacts, and sector-specific caution (office, construction).

- Banks with excess liquidity are pivoting toward consumer installment and secured lending but with lower credit appetite in indirect auto.

- Several management teams noted that new originations are now almost entirely sponsor-driven or pre-screened renewal business, with minimal new-to-bank volume.

Outlier Strategies: Beyond the Consensus

Not all banks are merely tightening the screws. A few have taken more radical approaches:

- Eagle Bancorp, Inc. aggressively reclassified and sold down $121 million of office loans, taking a one-time $113 million provision to reset its portfolio.

- Banc of California went further, explicitly avoiding entire sectors such as office lending, declaring “we don’t feel the need to be an office lender.”

- Provident Financial Holdings took the opposite path—loosening multifamily underwriting back to pre-COVID levels to grow volume.

These contrarian moves underscore the sector’s de-averaging: banks are no longer marching in macro lockstep but are making micro-strategic credit decisions based on capital, confidence, and geography.

Illustrative Quotes:

Atlantic Union Bankshares reported modest but quality-focused commercial loan growth, adding:“Loan growth remains disciplined, driven by existing customer expansion rather than new relationships.”

“Loan growth is positive but deliberate—every dollar must clear both profitability and risk hurdles.” — Pinnacle Financial Partners

“Core C&I pipelines remain healthy, though we’re prioritizing existing client expansion rather than new relationships.” — Hancock Whitney

“Loan-to-deposit ratios are normalizing, but we’re balancing yield with liquidity.” — Trustmark Corporation

“Loan pipelines are moderating, particularly in C&I, as clients remain cautious on expansion. We are seeing high-quality opportunities, but overall demand is clearly softer than a year ago.” – Wintrust Financial

“We are projecting low-single-digit loan growth for 2026, driven primarily by our specialized verticals. Paydowns in C&I are offsetting new origination volume, and new CRE origination is functionally at a standstill outside of select industrial.”- Associated Bancorp

The consensus is clear: loan growth is no longer a given. It will be a “fight for quality” in 2026, with net portfolio growth remaining anemic for most institutions as they focus on balance sheet defense over asset growth.

Section 3: Commercial Real Estate (CRE)

CRE remains the most polarized portfolio category.

Office: This segment has moved from a “problem” to a “workout” category. The analysis has fundamentally shifted from the asset to the sponsor. Banks are stating that the asset’s cash flow is, in many cases, insufficient. The new underwriting question is: Does the sponsor have the external liquidity and willingness to fund cash-flow shortfalls and tenant improvements?

- Zions Bancorporation noted: “Our focus remains on our CRE Office portfolio… We are finding that sponsor strength and willingness to inject fresh equity is the primary determinant of a loan’s outcome.”

This stress is leading to the first meaningful emergence of Other Real Estate Owned (OREO) in years. However, dispositions are frozen. Multiple banks cited a significant bid-ask gap, with First Horizon noting “price discovery remains challenging,” meaning banks are unwilling to accept the low-ball offers available, leading to protracted workout timelines.

Multifamily: Remains stable but is normalizing. The primary watch item, noted by East West Bancorp, is “supply pressures in certain Sunbelt submarkets” that are flattening rent growth and stressing new construction pro-formas.

Industrial & Retail: These segments remain standouts. Industrial fundamentals are described as “exceptionally strong,” while retail, particularly grocery-anchored neighborhood centers, is performing well.

OceanFirst Financial Corp underscored the importance of sponsor strength and market segmentation in its CRE oversight, noting: “Office remains under pressure, but we see solid performance in industrial and retail segments—this is a credit cycle defined by sponsor selectivity.”

Construction: New project starts have slowed dramatically due to high rates and elevated costs. Banks’ focus has shifted from origination to “managing existing project budgets” and “monitoring completion timelines and interest reserves.” .Construction lending tightened considerably given cost inflation from tariffs on imported materials.

Section 4: Commercial & Industrial (C&I)

The C&I portfolio is facing a two-front war: high rates and margin compression.

Cadence Bank articulated this: “C&I fundamentals are solid, but we are monitoring our variable-rate loan book for any erosion in debt-service coverage ratios.”

The second front is margin compression, driven by external factors:

- Trade/Tariff Exposure: Banks with manufacturing portfolios, like Associated Banc-Corp, reported that “persistent tariff impacts are compressing margins for clients” in fabricated metals and component parts.

- Government Shutdown Effects: The brief Q3 shutdown served as a “micro-stress test.” F.N.B. Corporation noted “temporary cash flow disruptions for our government contracting clients,” which, while resolved, highlighted the vulnerability of this sector to policy dysfunction.

Banks emphasized tighter structures, quicker re-rating of stressed credits, and increased use of relationship monitoring tools. Sponsor-backed loans were scrutinized more deeply, as banks seek evidence of sponsor commitment before renewal or refinancing.

Section 5: Consumer / Retail Credit

Consumer credit is bending but not breaking. The consumer story is also one of de-averaging. While prime borrowers and mortgage holders are performing exceptionally well, stress is accelerating in the sub-prime and lower-FICO tranches.

- Hancock Whitney summarized the trend: “We saw a modest, expected rise in auto and unsecured consumer delinquencies… The consumer remains generally healthy, but we are seeing some stress at the lower end of the income spectrum.”

- Auto & Card: Delinquencies are normalizing back toward 2018-2019 averages, with losses concentrated in more recent, high-LTV auto vintages.

- Mortgage & HELOC: These portfolios remain pristine. The “lock-in” effect of low-coupon first-lien mortgages means homeowners are not moving and have high levels of embedded equity, making HELOC performance exceptionally strong.

Section 6: Niche and Emerging Exposures

The NDFI and fund-finance portfolios have emerged as high-attention areas. The concern is contagion. Banks are well-collateralized at the fund level, but they have limited visibility into the performance of the funds’ underlying, illiquid assets. Synovus Financial and Comerica described enhanced monitoring of capital call and subscription line facilities. Primis Bank and Oriental Bank both acknowledged tighter risk oversight on specialized portfolios, with management citing enhanced counterparty analytics and field audits.

“We are deepening our due diligence and monitoring across all non-depository and specialty finance exposures.” — Primis Bank

Synovus Financial detailed its “rigorous monitoring of counterparty risk” in this space, noting that while their lines are performing, a failure of a large NDFI “represents a key systemic risk to monitor.” Concerns center on leverage opacity and illiquidity of underlying assets. This has prompted board-level reviews and stricter collateral verification practices. Banks are also moderating construction loan origination amid rising costs and slower project completion.

Section 7: Fraud, Controls, and Credit Convergence Convergence

A notable and concerning theme this quarter was the rise in commentary related to fraud-related operating losses and credit problems. As economic conditions tighten, fraud (from both external parties and internal borrowers) historically increases.

Banks are reporting upticks in everything from sophisticated check and wire fraud to outright borrower misrepresentation.

Fraud-related losses were most concentrated in asset-backed and NDFI portfolios, echoing incidents reported by Zions Bancorporation, Origin Bancorp, and Columbia Banking System. The patterns involve double-pledged collateral and falsified borrowing bases.

Some banks, like BOK Financial, mitigated this risk through technical verification systems such as MERS for all mortgage-backed collateral—an example of how operational risk management and credit risk oversight are converging.

Key Narrative Points:

- Multiple banks reported isolated but material fraud-related charge-offs, particularly in lender-finance and NDFI portfolios (double-pledged collateral, falsified borrowing bases, fund misreporting).

- The most affected institutions were mid-tier regionals expanding into high-yield, non-depository, or fintech-adjacent lending.

- Fraud incidents have accelerated the integration of operational risk into credit governance, with more banks shifting fraud analytics and third-party verification under the Chief Credit Officer’s purview.

- Some banks acknowledged that legacy monitoring systems could not detect real-time anomalies.

- Investment is increasing in AI-enabled transaction screening and daily covenant compliance reporting.

Illustrative Quotes:

“We experienced a small but notable fraud event in a lender-finance relationship; we’ve since upgraded verification protocols.” — Origin Bancorp

“Fraud losses are now treated as credit losses—governance is no longer a separate discussion.” — Zions Bancorporation

“operating losses from fraud, particularly sophisticated check and wire fraud schemes aimed at our commercial clients, have increased. We are investing heavily in new monitoring technology and client education to counter this trend.”- Synovus Financial

“as part of our enhanced portfolio review, we uncovered two instances of borrower fraud in our construction portfolio, where draws were requested for uncompleted work. This has led to a full-scale review of our construction lending controls and field audit processes.” – Columbia Banking System

OceanFirst Financial commented on operational vigilance, stating:

“Fraud and cybersecurity controls are now core to our credit discussions—we’ve built this into portfolio governance.”

Primis Bank echoed this integration, noting that technology investments have “improved early anomaly detection and shortened our response cycles.”

This rise in fraudulent activity reinforces the need for “boots-on-the-ground” credit management, including more frequent field audits for ABL and construction lines and heightened vigilance from treasury management teams.

Normalization is no longer hypothetical—it’s underway. The consensus view is that 2026 will see credit costs reverting toward long-run averages, driven by borrower-level downgrades and selective impairments rather than broad CECL overlays. Commerce Bancshares and others noted overhauls of internal risk-rating systems to better anticipate sponsor weakness and regional vacancy pressures.

Section 8: Cross-Sector Themes & 2026 Outlook

Normalization is no longer hypothetical—it’s underway. The consensus view is that 2026 will see credit costs reverting toward long-run averages, driven by borrower-level downgrades and selective impairments rather than broad CECL overlays. Commerce Bancshares and others noted overhauls of internal risk-rating systems to better anticipate sponsor weakness and regional vacancy pressures.

The 2026 outlook is defined by managing known problems.

Proactive Downgrades: The “pass-to-special mention” migration is the key risk management strategy. This is not a sign of panic but of a planned “pulling forward” of risk identification.

CECL Evolution: The 2023-2024 era of broad, macro-driven CECL builds is over. The 2026 outlook is for provisions driven by specific impairments as proactive downgrades crystalize into losses.

Sponsor Reliance: This theme is now universal. The strength of the sponsor is the primary mitigating factor in all stressed commercial asset classes.

OREO Strategy: The “bid-ask gap” in CRE-Office means banks must develop a clear strategy for OREO dispositions. This will be a slow, capital-intensive process of “work-and-hold” rather than a quick “dump-and-run.”

Technology and Governance: The Quiet Enabler – Beneath the credit headlines, banks are investing in foundational modernization—core system conversions, data integration, and AI-assisted analytics. First Internet Bancorp and Banc of California have tied technology directly to productivity and early-warning credit identification, signaling that digital infrastructure is now a core part of credit risk resilience.

Trade Impact: The margin squeeze from tariffs is now considered a permanent fixture in C&I underwriting, not a temporary headwind.

Section 9: Strategic Priorities for 2026

The 3Q25 results mark the end of an era in which benign credit conditions could mask structural weaknesses. The coming cycle will test credit cultures, governance frameworks, and the depth of analytical foresight across regional and community banks. Institutions that respond with agility—embedding data, discipline, and dialogue—will emerge stronger.

Beyond credit cycle management, the next frontier for regional and community banks will be operational readiness and modernization. The move by OceanFirst Financial Corp to outsource core residential underwriting exemplifies the expanding need for vendor governance frameworks. Similarly, banks nearing the $10 billion and $100 billion thresholds are seeking expert guidance on ERM, CECL, and stress testing programs.

Actionable Priorities for 2026

- Develop a Sponsor-Reliance Scorecard: Move beyond asset-level analysis in CRE. Rank every major sponsor across liquidity, leverage, and historical support. In an environment of elevated refinancing risk, sponsor quality is collateral.

- Reframe C&I Stress Testing: Integrate tariff-driven margin compression and working-capital stress into rate sensitivity tests. Focus on debt-service resilience, not just rate shocks.

- Audit and Fortify NDFI Exposure: Conduct comprehensive reviews of all fund-finance and capital call lines. Implement “look-through” analysis to identify embedded leverage and cross-collateralization risk.

- Modernize Risk-Rating Frameworks: If your system identifies weakness only after delinquency, it is already late. Integrate early-warning triggers—borrowing-base volatility, sponsor cash erosion, and covenant utilization—to surface risk migration preemptively.

- Build an OREO Disposition Strategy: Treat OREO as a strategic, not incidental, outcome. Model capital impacts, timeline liquidity paths, and coordinate asset management, tax, and legal planning before balances rise.

Closing Perspective: Credit Maturity, Not Credit Crisis

The 3Q25 earnings season confirms that U.S. banking is entering a phase of credit maturity—where discipline, governance, and granularity separate resilience from exposure.

Banks are not facing systemic deterioration, but rather a return to fundamentals: hands-on relationship management, forward-looking provisioning, and sponsor accountability.

Atlantic Union Bank and OceanFirst Financial both stressed the need for data-driven credit monitoring.

“We’re focused on enhancing portfolio analytics to anticipate migration before it shows in delinquencies,” Atlantic Union’s management said, aligning with the industry’s pivot toward predictive early-warning systems.

For credit leaders, this environment is not one to fear, but to master.

Those who invest now in predictive analytics, fraud governance integration, and proactive risk-rating modernization will not only withstand the next cycle—they will define it.