The Credit Normalization Handbook

Executive Credit Brief: What “Normalization” Means for 2026

Bottom Line:

The widely anticipated post-pandemic credit collapse did not materialize. Instead, banks are entering a period of credit normalization—a return to historical loss behavior, accompanied by sharply divergent risk across borrower size, sector, and underwriting discipline.

Three implications for Credit Committees in 2026:

- Normalization ≠ benign: Loss rates drifting back to 15–40 bps are not stress events—but misinterpreting them as such can lead to over-tightening and missed opportunities.

- Risk is now idiosyncratic, not systemic: Credit deterioration is concentrated in specific pockets—small C&I, discretionary sectors, SBA vintages, and operationally complex credits.

- Structure matters again: As competition intensifies for “safe” large C&I borrowers, the primary risk shifts from the probability of default to structure slippage and covenant erosion.

What Credit Officers should do differently this year:

- Re-anchor risk ratings, stress tests, and portfolio triggers to normalized loss expectations, not crisis benchmarks.

- Re-underwrite vulnerable portfolios (small business, SBA, discretionary sectors) with forward-looking cash-flow realism, not backward-looking performance.

- Treat AI exposure and disruption risk as a formal underwriting variable, not a qualitative footnote.

This handbook translates earnings commentary and January 2026 SLOOS data into actionable credit guidance for CCOs, portfolio managers, and credit committees navigating 2026.

Navigating the Split Screen: “Benign” for the Big, “Bumpy” for the Small

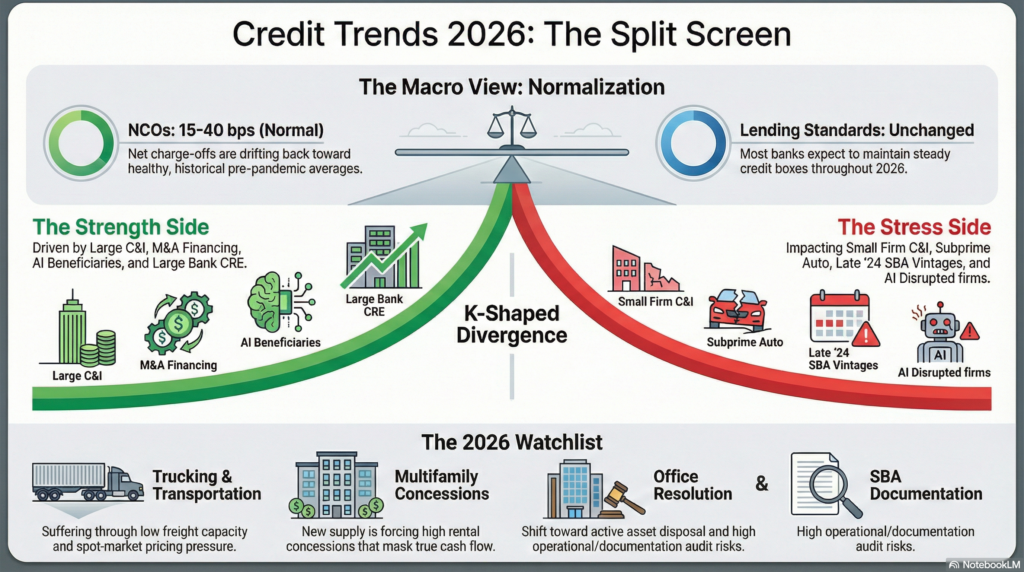

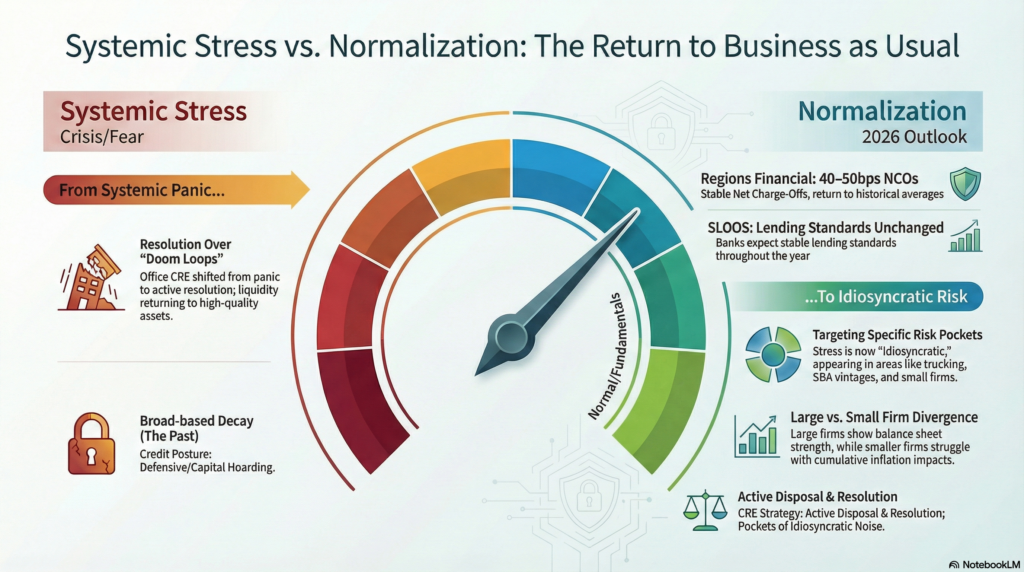

If the 2023–2024 banking narrative was defined by fears of systemic credit stress, the emerging message from 4Q25 earnings calls and the January 2026 Senior Loan Officer Opinion Survey (SLOOS) is markedly different: the industry is normalizing, not deteriorating.

That normalization, however, is uneven. Credit performance is increasingly K-shaped, with large and middle-market borrowers stabilizing or expanding, while smaller borrowers and select discretionary sectors absorb the cumulative impact of higher rates, inflation, and operational strain.

For credit committees, the challenge in 2026 is no longer identifying systemic stress—but correctly distinguishing normal loss behavior from emerging idiosyncratic risk.

1. Systemic Stress vs. “Normalization.”

For purposes of this analysis, credit normalization means a return to historical loss behavior and underwriting discipline, not a loosening of standards.

Normalization has four distinct dimensions:

- Loss Rates: Net charge-offs reverting toward long-term averages (approximately 15–40 bps for many portfolios).

- Risk Migration: Gradual criticized/classified movement driven by sector and size, not broad portfolio decay.

- Structure Discipline: Renewed importance of pricing, covenants, guarantees, and documentation quality.

- Credit Exceptions: Fewer pandemic-era accommodations; greater intolerance for weak structure masked by liquidity.

Mislabeling normalization as stress leads to defensive over-tightening. Mislabeling it as benign leads to complacency.

The consensus among regional bank executives is that asset quality remains robust, though metrics are naturally drifting up from historic lows. It is vital for credit committees to distinguish between a broken market and a normalizing one.

The Earnings View: Net Charge-offs (NCOs) and Non-Performing Assets (NPAs) are ticking up, but executives consistently characterize this as “noise” or “cleanup” rather than a trend of decay.

- Regions Financial noted that “Credit quality or the deterioration in credit quality peaked a couple of quarters ago,” and they expect full-year 2026 NCOs to settle between 40 and 50 basis points.

- Ameris Bancorp anticipates NCOs in the 20-25 basis-point range, viewing this as a healthy normalization.

- Old National Bancorp actually reported an “8% reduction in total criticized and classified loans”.

The SLOOS Validation: January 2026 SLOOS confirms this stability. Banks reported that they “expect lending standards generally to remain unchanged” through 2026. This lack of aggressive tightening signals confidence.

- The Nuance: While standards are stable, banks are “reluctant to loosen”. During 4Q25, banks actually “tightened for C&I and subprime mortgage”, reinforcing that while the crisis is over, the credit box remains guarded.

Strategic Takeaway: Credit Officers should avoid over-tightening credit boxes in response to headline noise. A return to 15–40 bps NCOs is not a crisis; it is the cost of doing business. However, as the SLOOS data suggests, maintaining discipline in C&I standards is prudent given the economic uncertainty.

Credit Committee Actions – Systemic vs. Normalized Environment

- Re-baseline expected loss ranges in portfolio monitoring dashboards.

- Avoid risk-rating inflation solely due to NCO normalization.

- Maintain discipline in C&I underwriting, particularly where borrower cash-flow resilience remains unproven.

2. The K-Shaped Recovery: Small vs. Large Firm Dynamics

Perhaps the most critical takeaway for 2026 is the divergence between small and large borrowers.

Small Firms (The Stress Point): Smaller entities are struggling to absorb the cumulative impact of higher rates and inflation. They lack the pricing power to pass on costs, leading to rapid margin compression.

- Earnings Red Flag: First Bank was blunt, stating that “delinquency and charge-offs exceeded what we believe to be accessible levels” in its small-business products.

- SLOOS Warning: SLOOS indicates that banks are specifically eyeing “C&I to small firms” for deterioration. While large-firm credit quality is expected to remain unchanged, a “moderate net share of banks reported expecting a deterioration for C&I loans to small firms.”

- Demand: Again, based on SLOOS data, Demand from small firms remained “basically unchanged,” indicating limited investment appetite or capacity.

Large/Middle Market Firms (The Growth Engine): Conversely, banks serving larger C&I clients are experiencing stability and aggressive growth.

- Earnings Strength: Huntington Bancshares reported robust loan growth driven by “corporate and specialty banking”. KeyCorp saw C&I outstandings increase by $900 million, driven by broad-based growth.

- SLOOS Optimism: Banks reported improved demand for C&I loans to large firms—the “best reading in 3.5 years”. The drivers are positive: “increased customer financing needs for M&A, for inventory, and for investment in plant or equipment”.

Strategic Takeaway: The risk in 2026 lies in the “middle.” As banks rush to pivot toward these “safe” large C&I borrowers, competition is heating up. Colony Bank noted “increased competition in lending”. When the entire industry pivots to the same asset class (Large C&I), structure slippage often follows pricing compression.

Credit Actions: Managing the K-Shaped C&I Market

- Small C&I (<$50MM revenue):

- Stress-test margins for inability to pass through inflation.

- Scrutinize reliance on deferments, interest-only periods, or covenant relief.

- Large / Middle-Market C&I:

- Heighten focus on structure as competition increases.

- Monitor covenant dilution and sponsor leverage creep.

- Portfolio Risk:

- The greatest 2026 risk lies in the “middle”—credits that appear stable but are underwritten on optimistic assumptions.

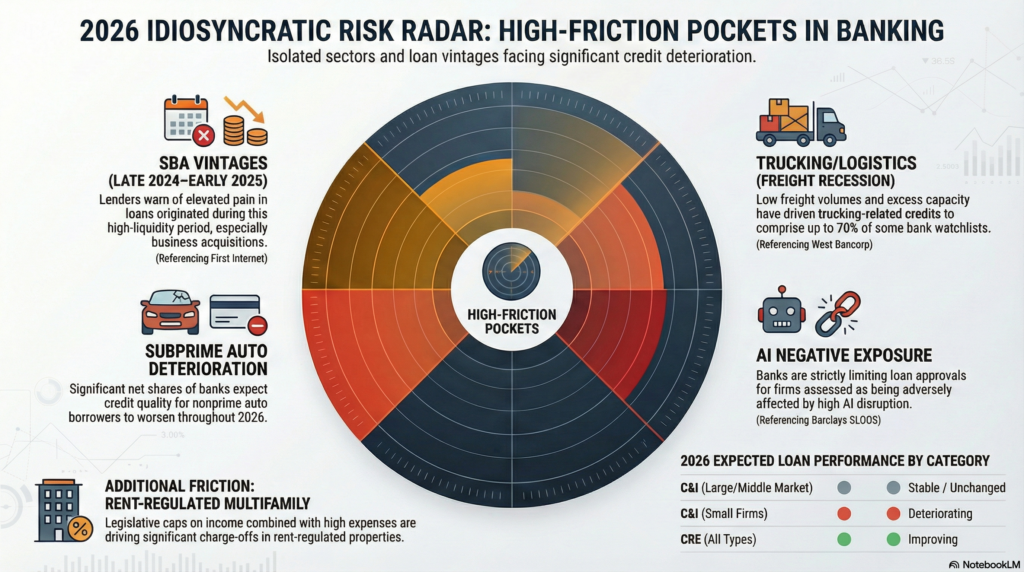

3. Discretionary & Niche Sector Risks: The “Idiosyncratic” Flares

If systemic risk is low, where is the pain? The earnings transcripts pinpoint specific verticals—mostly discretionary or operationally complex—where higher rates are cracking the foundation.

A. Trucking & Logistics The freight recession continues to drag on C&I portfolios.

- West Bancorporation revealed that “70% of our watch list is related to the trucking industry,” citing low freight and excess capacity.

- Enterprise Financial took an $8.5 million charge on a logistics company where the “growth rate outstripped its capital”.

B. Discretionary Consumer Spending (Wine & Powersports) Sectors dependent on non-essential consumer spending are showing strain, suggesting the consumer wallet is tightening.

- Bank of Marin downgraded a wine-industry credit due to declining cash flows and visitation, noting that the industry is “going through its own struggles”.

- Old Second Bancorp reported higher gross charge-offs in its Powersports business, though it noted that yields compensate for the risk.

C. Franchise Finance

- South Plains Financial took a $6 million charge-off on a franchise loan where “the franchisee and the franchisor could not find an agreeable path forward”. This highlights the “Brand Risk” in franchise lending—if the franchisor falters or disputes arise, the unit economics crumble.

D. Consumer & Auto (The SLOOS Warning) While earnings were mixed on consumer health, the Barclays report is bearish.

- Outlook: Banks expect asset quality “to deteriorate for resi R/E and most consumer loan categories” in 2026.

- Auto Loans: Significant net shares of banks expect deterioration in credit quality for “auto loans to nonprime borrowers”.

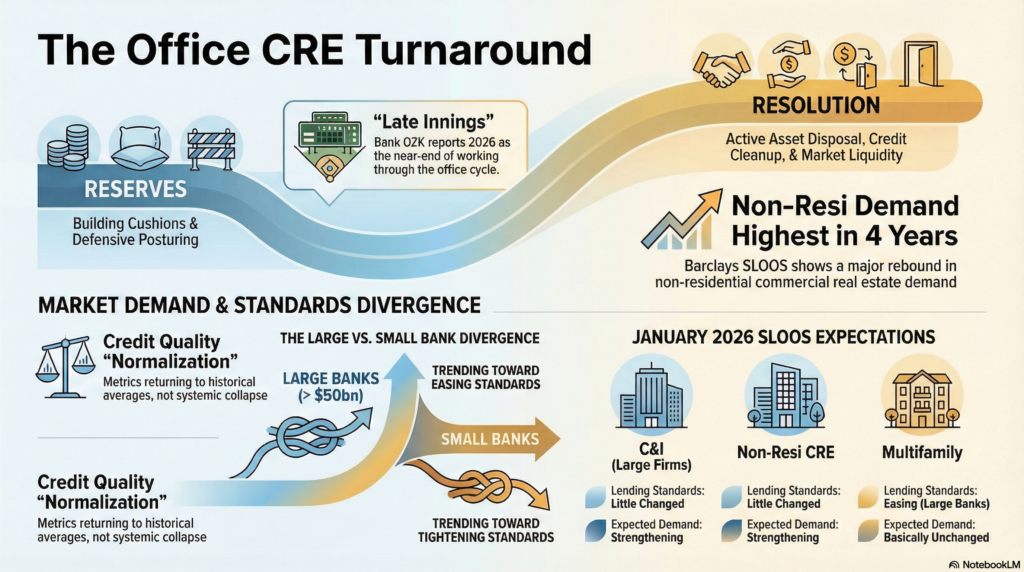

4. Handling the “Tail End” of the Office CRE Cycle

The narrative on Office CRE has shifted from “panic” to “resolution.” Banks are no longer just building reserves; they are actively disposing of assets.

The “Late Innings” View: Bank OZK, a major player in the space, stated that it believes the industry is “pretty near the end of working through that cycle”. Western Alliance was explicit: “We expect net charge-offs to remain elevated in the first half of the year as we work through nonaccrual loans”.

The “Green Shoots” from SLOOS: Contrary to the “doom loop” narrative, the SLOOS report highlights that banks expect “credit quality to… improve for CRE loans” in 2026.

- Demand is Back: Banks reported the “highest reading [in] 4 years” for non-farm non-residential CRE demand.

- The Size Split: However, there is a divergence. Large banks (>$100bn assets) reported “having eased” CRE standards, while smaller banks “tightened standards”.

5. Where Banks Are Most Likely to Get This Wrong in 2026

- Over-tightening small business credit and accelerating adverse selection.

- Chasing “safe” large C&I borrowers while conceding pricing and structure.

- Treating SBA guarantees as substitutes for underwriting discipline.

- Ignoring operational risk as a driver of realized credit losses.

- Viewing AI exposure as theoretical rather than underwriting-relevant.

6. SBA Vintages: The “Hidden” Risk

SBA portfolios originated during periods of excess liquidity and rapid growth—particularly late 2024 through early 2025—warrant targeted re-review. Recent earnings commentary highlights that losses are emerging not from credit weakness alone, but from operational and documentation failures that impair the recoverability of guarantees.

SBA Credit Review Priorities

- Re-review the late-2024 and early-2025 vintages for deferment reliance and early-payment stress.

- Validate equity-injection documentation and lien perfection for recent originations.

- Segment unguaranteed exposure separately in portfolio analytics.

- Treat SBA operational compliance as a credit risk variable, not a back-office issue.

Vintage Risk: First Internet Bancorp warned that there “may be more pain to come,” specifically in SBA loans originated in “late 2024 and early 2025”.

- Unguaranteed Exposure: BayFirst Financial reported elevated charge-offs in unguaranteed SBA 7(a) loans, noting that stricter servicing standards led to accelerated classification of loans.

- Operational Risk: South Plains Financial disclosed a charge-off due to a “documentation error in the underwriting” that led them to forgo pursuing the guarantee—a reminder that in high-volume environments, technical errors can translate into credit losses.

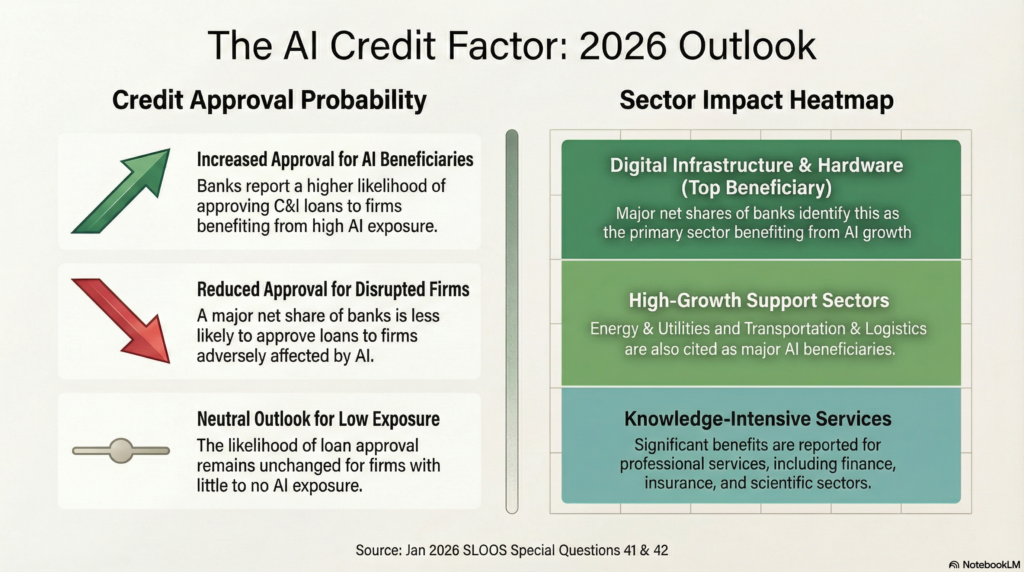

6. The AI Factor: The New “Binary” in Underwriting

The January 2026 SLOOS introduced a new, critical variable into the credit decisioning matrix: Artificial Intelligence Exposure. For the first time, the Federal Reserve explicitly queried banks on how AI impacts credit availability, and the results describe a “binary” outcome where AI exposure acts as either a supercharger or a disqualifier.

The “Approval Gap”: Credit committees are no longer neutral on technology. The survey data reveals a sharp divergence in appetite based on a borrower’s relationship with AI:

• The “AI Premium”: A moderate net share of banks reported they are more likely to approve C&I loans to firms “benefiting from high AI exposure” compared to the beginning of 2025.

• The “AI Penalty”: Conversely, a major net share of banks reported being less likely to approve loans to firms “adversely affected by high AI exposure.”

• The Baseline: For firms with “little exposure” to AI, approval standards remained largely unchanged.

Strategic Implication: This suggests that “Disruption Risk” is now a formal underwriting criterion. Borrowers who cannot articulate an AI defense strategy may face a silent tightening of credit terms, regardless of their current cash flow.

Governance Implication

AI exposure now functions as an underwriting variable comparable to customer concentration or supplier dependency. Credit policies and credit memos should explicitly document:

- Whether AI is a tailwind, neutral factor, or structural threat to the borrower’s business model.

- How AI-related disruption risk is reflected in stress testing, tenor, pricing, and covenants.

Sector Winners & Losers: The survey also asked banks to rate the impact of AI on specific borrower sectors. The consensus views AI as a net positive for operations, but specifically favored capital-intensive and logistical industries:

• Digital Infrastructure & Hardware: View as the top beneficiary. Banks cited this sector most frequently as experiencing “beneficial effects,” signaling a strong appetite for lending to data centers, chip manufacturers, and supporting infrastructure.

• Energy & Utilities: Also rated highly beneficial, likely driven by the increased power demand from AI computation (data centers), making utility capex a favored lending category.

• Transportation, Logistics, & Commerce: Banks see AI driving efficiency here, supporting credit quality.

• Professional Services: Knowledge-intensive sectors are viewed as beneficiaries, likely due to margin expansion from efficiency gains.

Actionable Strategy: Credit Officers should add an “AI Impact Assessment” to the credit memo for all C&I borrowers with revenue>$10MM.

1. Defensive Check: Does the borrower’s business model rely on labor arbitrage that AI could commoditize (e.g., BPO, basic coding, transcription)? If yes, stress test revenue down 15-20%.

2. Offensive Check: Is the borrower requesting capex for AI integration? If yes, treat this as a “modernization” expense, similar to ERP upgrades—essential to preserving enterprise value.

Actionable Insight: The Idiosyncratic Risk Checklist

Based on the specific “one-off” issues cited in Q4 earnings and the forward-looking SLOOS data, Credit Officers should run their portfolios against this checklist.

| West Bancorp noted that trucking comprises 70% of its watchlist. | The “Red Flag” Indicator | Context from Earnings & SLOOS |

|---|---|---|

| Small Firm C&I | Margin Compression: Review borrowers with <$50MM revenue who cannot pass on inflation costs. | SLOOS: Explicit expectation of credit quality deterioration for small firms. |

| SBA Vintages | Late 2024 – Early 2025: Specifically review payment habits and deferment reliance in these vintages. | First Internet Bancorp flagged these vintages as having higher potential for pain. |

| Logistics/Trucking | Spot Market Reliance: Stress test cash flows against a “low freight” scenario. | West Bancorp noted trucking comprises 70% of their watchlist. |

| Discretionary Spend | Luxury/Leisure: Review exposure to wineries, powersports, or high-end leisure. | Bank of Marin & Old Second noted stress in wine and powersports. |

| SBA Operations | Documentation Audit: Verify equity injection proofs and lien perfections on top 20 recent SBA originations. | South Plains took a loss due to a documentation error voiding the guarantee. |

| Multifamily | Concession masking: Review properties in lease-up. Are DSCRs based on collected or contract rents? | Texas Capital noted projects require concessions to maintain occupancy, impacting NOI. |

| AI Disruption | Business Model Threat: Screen borrowers in sectors “adversely affected by high AI exposure.” | SLOOS: Banks are “less likely to approve loans” to firms negatively impacted by AI. |

The Bottom Line for Credit Leaders

The “Great Credit Crash” has been replaced by a Great Credit Normalization. Losses are returning to historical ranges, not accelerating into crisis. However, normalization is uneven and unforgiving.

Large borrowers are entering a renewed growth phase driven by M&A and capital investment. Smaller borrowers, discretionary sectors, and operationally complex credits continue to face pressure. The risk in 2026 is not systemic—it is misclassification, mis-structuring, and misinterpretation.

Credit leaders who recalibrate frameworks, not just thresholds, will be best positioned to manage risk—and capture opportunity—in the next phase of the cycle.