From Defense to Offense: Key Takeaways from 4Q25 Regional Bank Earnings

By Amitabh Bhargava

After a year defined by balance sheet optimization and defensive posturing, the narrative across the regional and community banking sector shifted significantly in the fourth quarter of 2025. An analysis of earnings call transcripts from over 140 institutions reveals a sector pivoting toward cautious optimism for 2026.

While “normalization” remains the watchword for credit quality, executives are increasingly focused on organic growth, utilizing market disruption to acquire talent, and moving Artificial Intelligence (AI) from theoretical pilot programs to deployable efficiency tools.

Here are the critical takeaways for bankers and credit union executives from the Q4 2025 cycle.

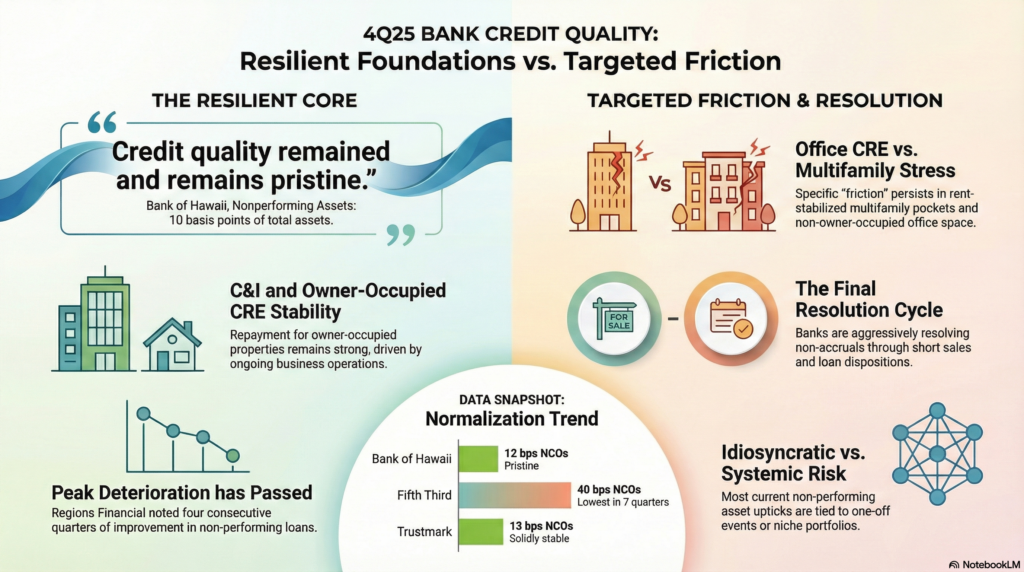

1. Credit Quality: The “Normalization” Narrative

The prevailing theme regarding credit is resilience. Despite fears of systemic stress, most institutions reported metrics that are normalizing from historic lows rather than spiraling. While Non-Performing Assets (NPAs) have ticked up in isolated pockets, executives emphasized that these issues are idiosyncratic rather than systemic.

• The CRE Outlook: Friction remains in Office CRE and specific Multifamily pockets, but many banks view 2026 as the final lap of this resolution cycle. For example, Bank OZK noted, “We think 2026 is another year like 2025 where we’re just working through the environment… we think 2026 is pretty near the end of working through that cycle”.

• Specific Stress Points: Banks identified friction in SBA portfolios and niche lending verticals like Powersports. First Internet Bancorp noted their credit issues were isolated to SBA and franchise finance, suggesting “more pain to come” as they work through loans originated under previous guidelines.

SLOOS Context: According to the January 2026 Senior Loan Officer Opinion Survey (SLOOS), banks expect asset quality to remain mixed in 2026. While they anticipate improvement in CRE credit quality, they expect deterioration in consumer loans (auto and credit card) and C&I loans to smaller firms.

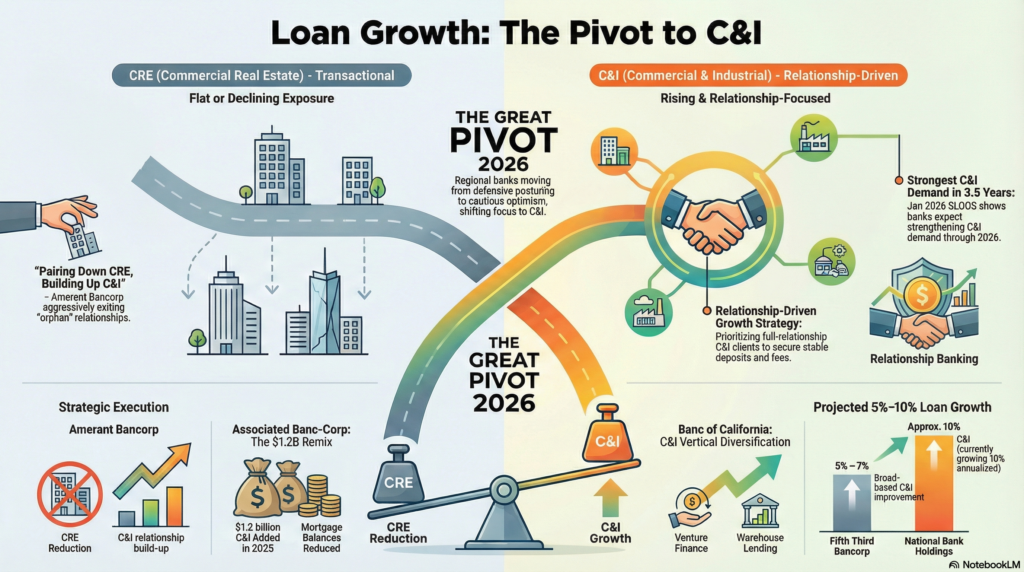

2. Loan Growth: The Pivot to C&I

The consensus strategy for 2026 is a pivot to offense, specifically targeting Commercial & Industrial (C&I) lending over transactional Real Estate. Banks are guiding for mid-single-digit loan growth, fueled by full-relationship banking that captures deposits alongside credit.

• The Payoff Headwind: Headline growth numbers in Q4 were dampened by elevated payoffs. First Financial Bancorp reported a “record level of payoff activity,” up 56% over the prior quarter, which masked strong origination volumes.

• Relationship Focus: The goal is to avoid “orphan” loans. Amerant Bancorp stated explicitly: “We’re pairing down our CRE. We’re building up C&I, we don’t want orphan relationships. We want full relationships”.

SLOOS Context: The demand outlook supports this pivot. The SLOOS indicates that significant net shares of banks expect stronger demand for C&I loans in 2026, driven by declining interest rates and increased customer financing needs for M&A and inventory

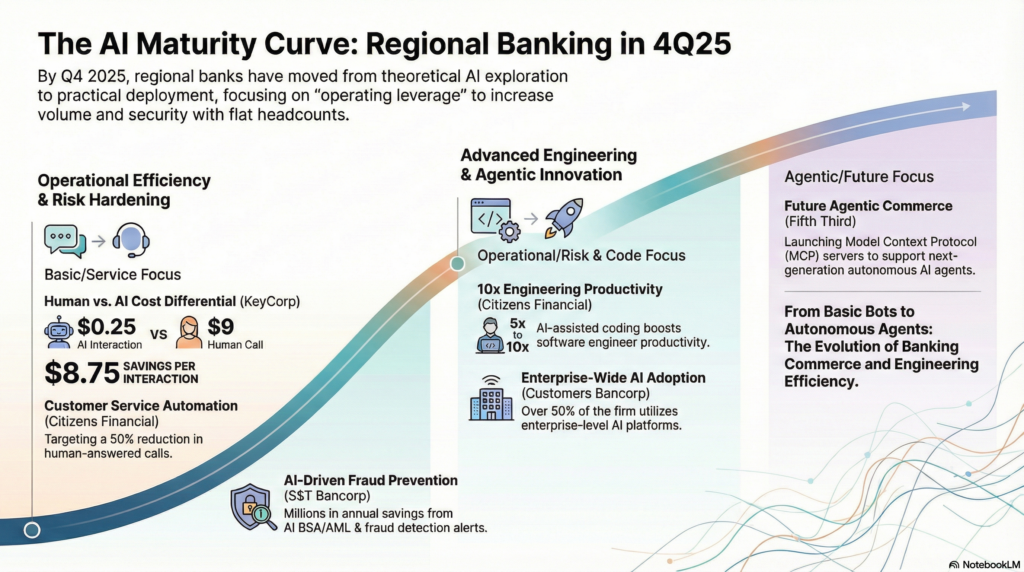

3. AI Utilization: From Buzzword to Bottom Line

The discussion on Artificial Intelligence has matured rapidly. It is no longer about novelty; it is about operating leverage and fraud prevention.

• Coding and Efficiency: Citizens Financial highlighted that AI is “taking the first crack at writing the code,” projecting a 5x to 10x productivity gain for engineers.

• Fraud Defense: S&T Bancorp noted that their Financial Intelligence group is AI-driven, creating alerts that are “worth millions of dollars of savings” by stopping fraud before it happens.

• Cost Reduction: KeyCorp provided a stark metric: “A call to a call center costs $0.25 using AI. And if a human picks it up, it costs $9”

4. Capitalizing on Disruption: The War for Talent

A distinctive theme in Q4 was the opportunity created by M&A among competitors. Regional banks are positioning themselves as beneficiaries of “creative destruction,” aggressively hiring displaced teams to drive organic growth.

• SouthState Bank noted that “$118 billion of bank deposits are going to go through a conversion in the next year,” creating a massive opportunity to win clients and talent during the disruption.

• Pinnacle Financial Partners described the market disruption as a “generational opportunity” for recruiting revenue producers

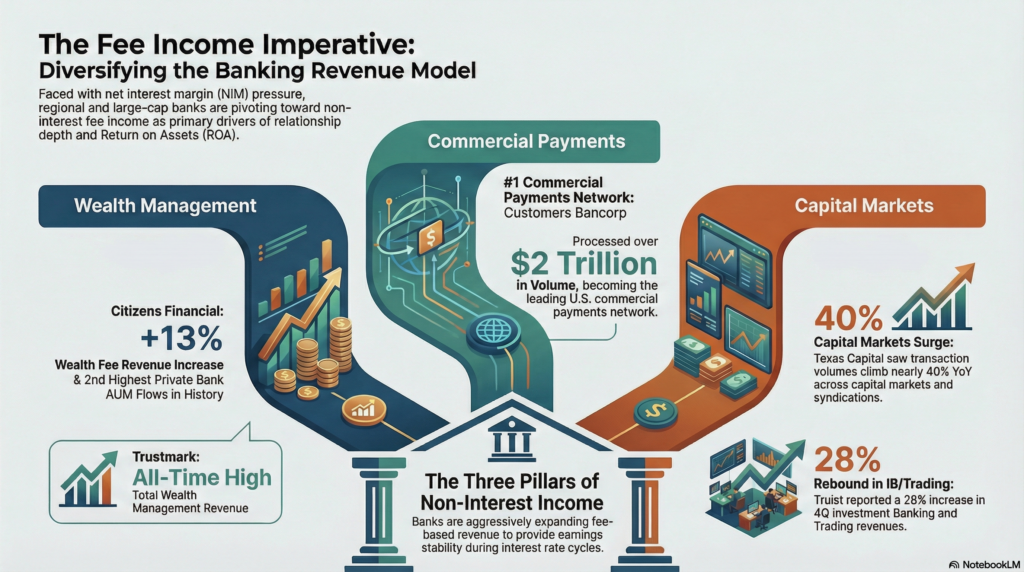

5. The Fee Income Imperative

With Net Interest Margin (NIM) stabilizing but still under pressure from deposit costs, banks are aggressively diversifying into fee-based revenue streams.

• Wealth & Payments: Customers Bancorp highlighted their success in payments, processing over $2 trillion in volume. Trustmark reported wealth management revenue reaching an all-time high.

• Capital Markets: There is a resurgence in capital markets activity. Texas Capital noted a nearly 40% year-over-year climb in transaction volumes across capital solutions and syndications

Conclusion: The 2026 Inflection Point

If 2025 was the year of “balance sheet fortification,” the fourth quarter signaled the beginning of the “great pivot” toward execution. The defensive crouch that defined the post-March 2023 era is ending, replaced by a cautiously optimistic offensive for 2026.

The data supports this shift. According to Barclays’ post-earnings analysis, the median bank grew EPS by 17% in 2025, and management guidance implies continued double-digit growth for 2026, driven by record revenues from rebounding net interest income and fee generation. This financial optimism is underpinned by the Federal Reserve’s January 2026 Senior Loan Officer Opinion Survey, which reveals that banks expect stronger loan demand across all categories in 2026—led specifically by the C&I and residential real estate sectors that regional banks are aggressively targeting.

However, a rising tide will not lift all boats equally. The widening gap between high-performing regionals and the rest of the pack will likely be defined by two non-financial factors: Technology and Talent.

1. The AI Dividend: Banks like KeyCorp and Citizens Financial are no longer just piloting AI; they are banking on it for material operating leverage, aiming for productivity gains that competitors relying on manual back-offices cannot match.

2. The Disruption Premium: As SouthState Bank and Pinnacle Financial noted, the “creative destruction” caused by competitor M&A has unleashed a “generational opportunity” to recruit top-tier revenue producers. The banks that win in 2026 will be those that successfully onboard this displaced talent to drive organic C&I growth.

As we move deeper into 2026, the narrative has moved beyond “surviving” the credit cycle to “thriving” in a normalizing economy. For bankers, the playbook is clear: leverage the stabilizing rate environment to capture demand, use market disruption to upgrade talent, and deploy technology to protect margins. The “normalization” is here; the race for market share has resumed.