Navigating the 2026 Energy Shock: Credit Risk Implications and How SRA Consulting Can Help

Executive summary

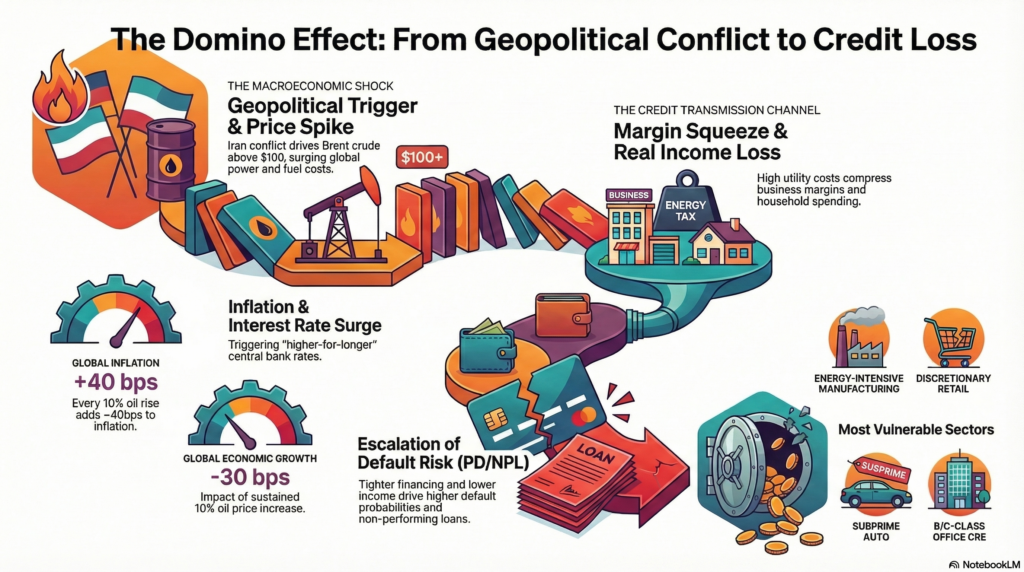

The 2026 Iran conflict has triggered a sharp rise in oil and gas prices, pushing Brent back above 100 dollars per barrel and lifting global power and fuel costs. The IMF estimates that a sustained 10 percent rise in oil prices adds about 40 basis points to inflation, while private‑sector analyses suggest the current shock could trim roughly 30 basis points from global growth and raise headline inflation by around half a percentage point over the next year. Central banks that were poised to ease are now signalling a higher‑for‑longer, and potentially higher‑still, rate path, prolonging tight financial conditions for leveraged borrowers. For banks and credit platforms, this represents a classic stagflationary test of credit processes, models, and monitoring.

Recent data suggests that credit risk has already been building beneath the surface, even as market spreads remained relatively benign. Internal bank risk ratings have shown a gradual increase in downgrades relative to upgrades among corporate borrowers in recent years, suggesting that underlying credit quality may be weaker than external pricing indicates.

In that context, an energy shock is less a standalone event and more a catalyst that accelerates existing vulnerabilities.

How the Energy Shock Transmits into Credit Risk

Energy shocks rarely impact credit directly—they transmit through margins, liquidity, and ultimately borrower behavior. The primary transmission channels include:

- Margin Compression: Higher fuel, input, and transportation costs reduce EBITDA, particularly in energy-intensive sectors such as transportation, chemicals, and manufacturing.

- DSCR Pressure: Even modest declines in EBITDA can push already-thin debt service coverage ratios below covenant thresholds.

- Working Capital Strain: Increased input costs require higher inventory and receivable financing, placing pressure on borrowing bases and revolver utilization.

- Liquidity Erosion: Borrowers may draw on revolvers earlier and more frequently, reducing cushion for unforeseen stress.

- Delayed Pass-Through: Many companies are unable to pass cost increases to customers immediately, creating timing mismatches that stress short-term liquidity.

These dynamics often emerge before headline deterioration in financial statements, making early identification critical.

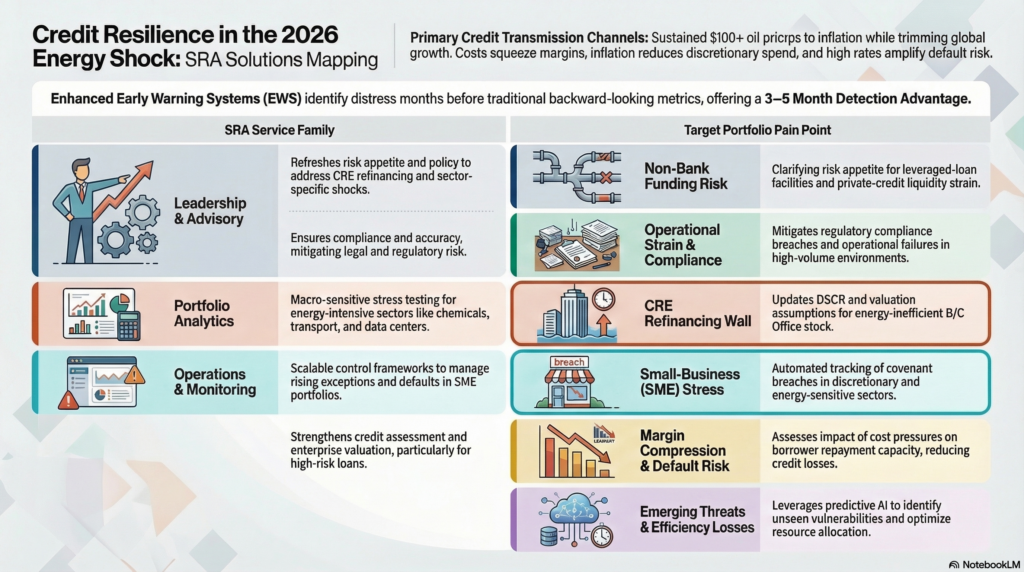

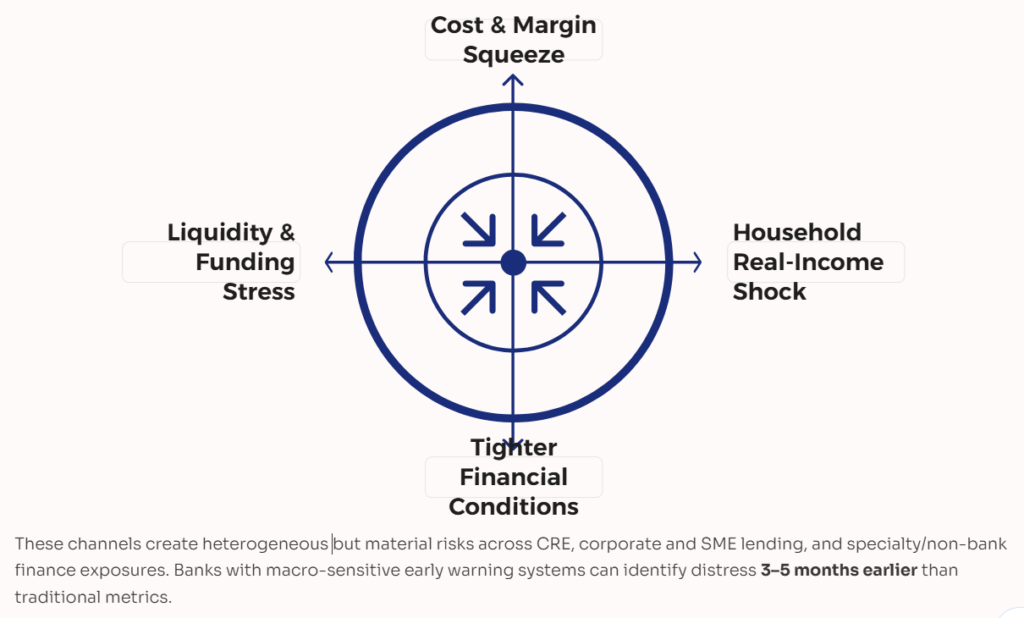

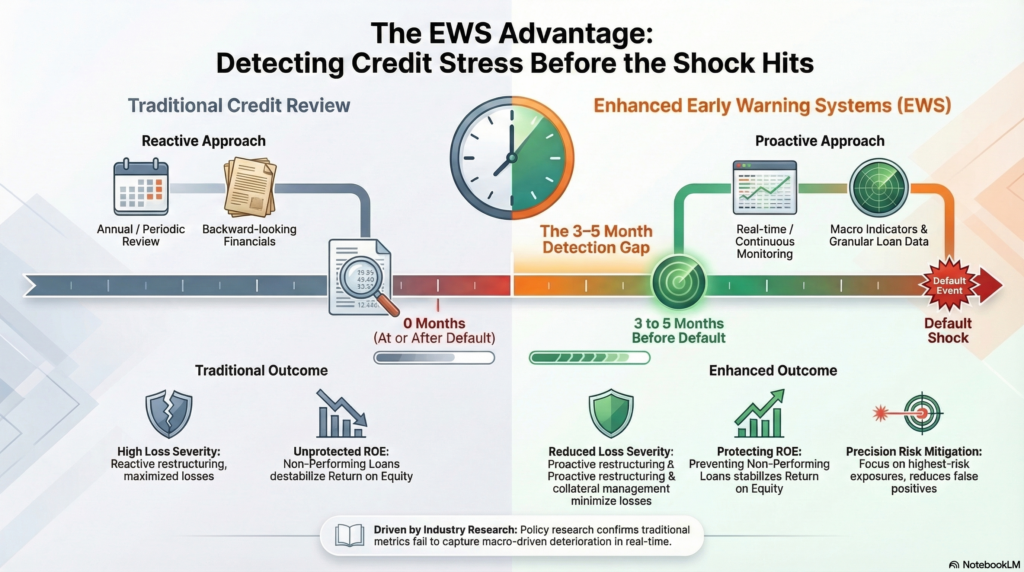

Recent work on early warning systems (EWS) shows that banks that integrate macro‑sensitive indicators and granular loan data can identify distress three to five months earlier than traditional metrics, enabling more effective risk mitigation and capital planning. Against this backdrop, SRA Consulting’s credit services—spanning leadership support, independent review, portfolio analytics, operations, underwriting, and innovation—are directly aligned to help institutions diagnose exposures, upgrade their credit toolkits, and execute a disciplined response.

Macroeconomic and sector context

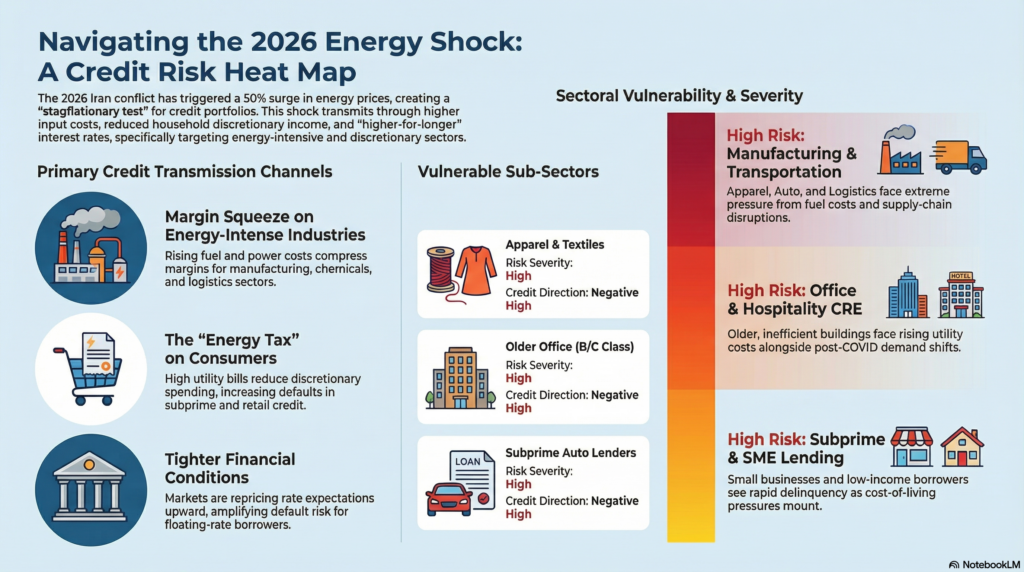

Oil and gas prices have surged more than 50 percent since the onset of the conflict in Iran, reflecting both supply-disruption risk and heightened risk premia. The IMF and other policymakers warn that a prolonged rise in energy prices will raise inflation and dampen growth, with the IMF using a rule of thumb that a sustained 10 percent rise in oil prices adds roughly 40 basis points to global inflation and reduces growth. Central banks in advanced and emerging economies have responded by holding or signalling higher policy rates, reversing earlier expectations of broad‑based cuts and maintaining pressure on real borrowing costs.

Analyses from multilateral institutions and academic work on macro shocks and NPLs show that such episodes tend to increase banking‑system credit risk over time, with default rates rising as higher financing and input costs erode coverage ratios and liquidity. For lenders, this environment increases the value of robust portfolio analytics, sector‑specific credit frameworks, and early warning capabilities.

Credit transmission channels

Energy shocks affect credit portfolios via several interconnected channels:

- Cost and margin squeeze: Higher fuel, power, and input prices compress margins for energy‑intensive industries (chemicals, metals, cement, data centers, cold‑chain logistics) and sectors where energy accounts for a meaningful share of operating costs (transportation, hospitality, restaurants, small retail).

- Household real‑income shock: Higher energy and food bills function as an “energy tax,” reducing discretionary spending and raising delinquencies in unsecured consumer credit, subprime auto, and small business segments.

- Tighter financial conditions: Markets are repricing rate expectations upward in response to the shock, and research on macro shocks and NPLs confirms that higher rates amplify default risk, particularly for floating‑rate and highly leveraged borrowers.

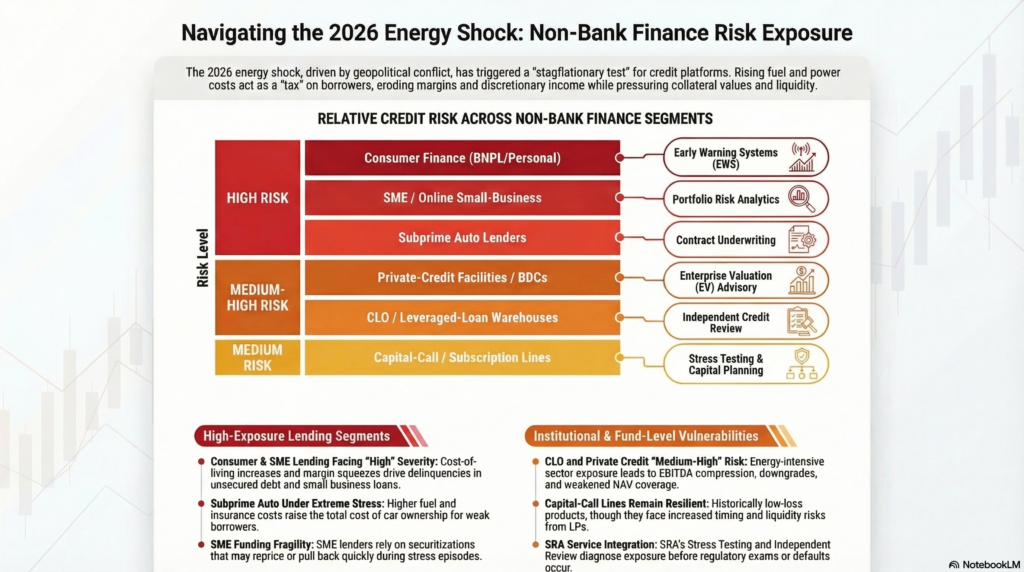

- Liquidity and funding stress for non‑banks: Recent episodes have highlighted the vulnerability of non‑bank financial intermediaries, including funds and finance companies, to margin calls and funding disruptions when volatility rises, and spreads widen.

These dynamics create heterogeneous but material risks across commercial real estate (CRE), corporate and SME lending, and specialty/nonbank finance exposures.

Key portfolio vulnerabilities for banks and credit platforms

Most Exposed Industry Groups (Prioritized View)

Not all sectors are equally impacted. Based on current conditions, risk is likely to emerge in tiers:

🔴 High Vulnerability

- Transportation (trucking, airlines, logistics)

- Chemicals and industrial manufacturing

- Energy-intensive processing industries

🟠 Moderate Vulnerability

- Consumer discretionary (margin sensitivity + demand elasticity)

- General manufacturing

- Construction and building materials

🟢 Relative Beneficiaries / More Resilient

- Energy producers

- Select utilities (with pass-through mechanisms)

- Infrastructure with contracted revenue models

This tiering is critical for portfolio segmentation and targeted credit review.

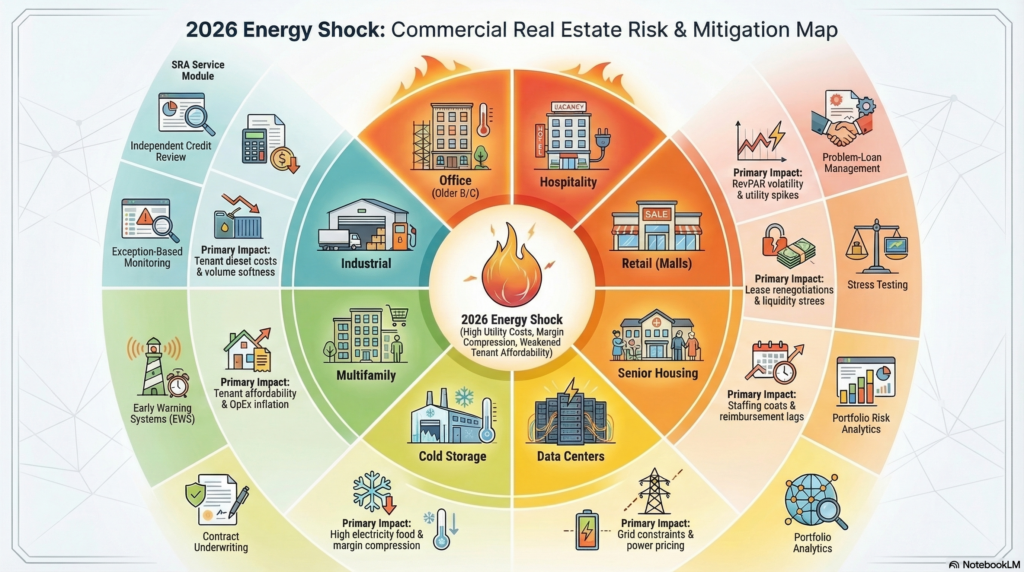

CRE performance is shaped by the interaction of energy costs, tenant health, and refinancing conditions. Office (particularly older B/C stock), hospitality, cold storage, and senior housing are among the more exposed asset classes because utilities and capex are significant relative to NOI and because demand fundamentals were already challenged in several of these sectors. Data‑center and AI infrastructure assets add a newer dimension: they are extremely power‑intensive, with higher electricity prices and grid constraints now viewed as central financial risks by investors and policymakers.

Multifamily and grocery‑anchored retail remain comparatively defensive, but face affordability constraints as tenants absorb higher rents on top of energy and food inflation, while small‑tenant retail and restaurant‑anchored strips are vulnerable to independent operator stress. For banks, the immediate priorities include updating DSCR and valuation assumptions for energy‑intensive property types, reviewing near‑term maturity walls, and linking tenant‑level early warning signals to property‑level risk grading.

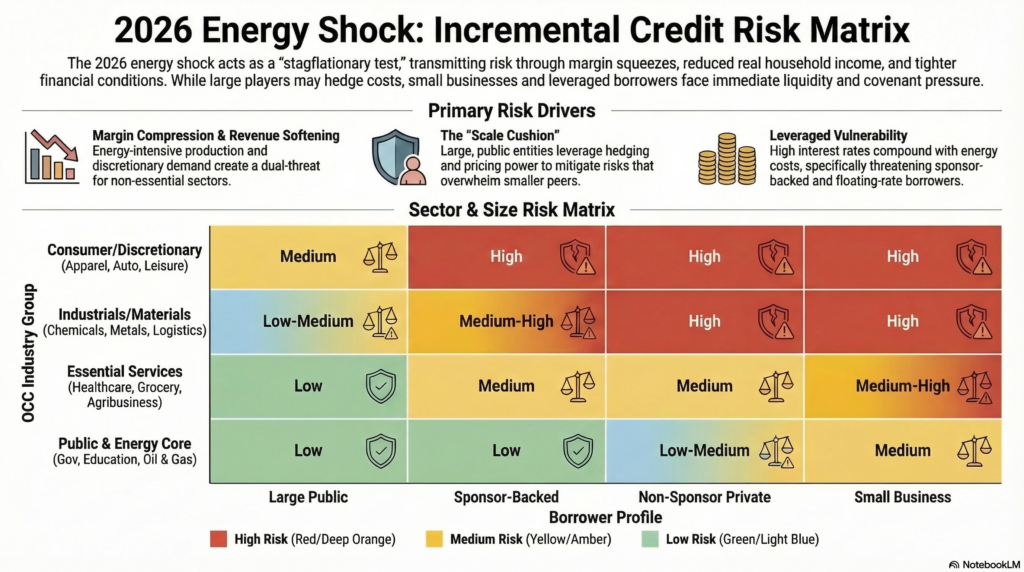

Corporate, SME, and specialty finance

On the corporate side, the greatest incremental risks are in energy‑intensive manufacturing and materials, transportation and logistics, and discretionary consumer sectors (apparel, mid‑tier restaurants, entertainment), particularly among non‑sponsor and small‑business borrowers with limited hedging and pricing power. Specialty‑finance exposures—consumer finance companies, subprime auto, SME online lenders, and marketplace/point‑of‑sale lenders—are vulnerable to rising delinquencies and widening of ABS spreads as household budgets come under pressure and funding costs rise.

Within institutional portfolios, CLO warehouses and leveraged‑loan facilities face mark‑to‑market and OC/IC test risk as spreads widen and downgrades accumulate in cyclical sectors, while fund‑level facilities to private‑credit managers and capital‑call lines to PE and infrastructure funds must be assessed for liquidity strain and collateral coverage in a more volatile environment.

What Breaks First in Credit Portfolios

Based on ongoing credit review experience, early signs of stress tend to appear well before formal downgrades:

- Covenant Cushion Erosion: Borrowers operating closer to minimum thresholds than reported

- Increased Revolver Utilization: Early signs of liquidity tightening

- Delayed Financial Reporting: Often a leading indicator of operational strain

- Sponsor Support Assumptions Weakening: Particularly in sponsor-backed middle market credits

- Working Capital Volatility: Inventory build and receivable stretch masking underlying stress

These signals are often visible at the loan level before they are reflected in portfolio metrics or criticized/classified migration.

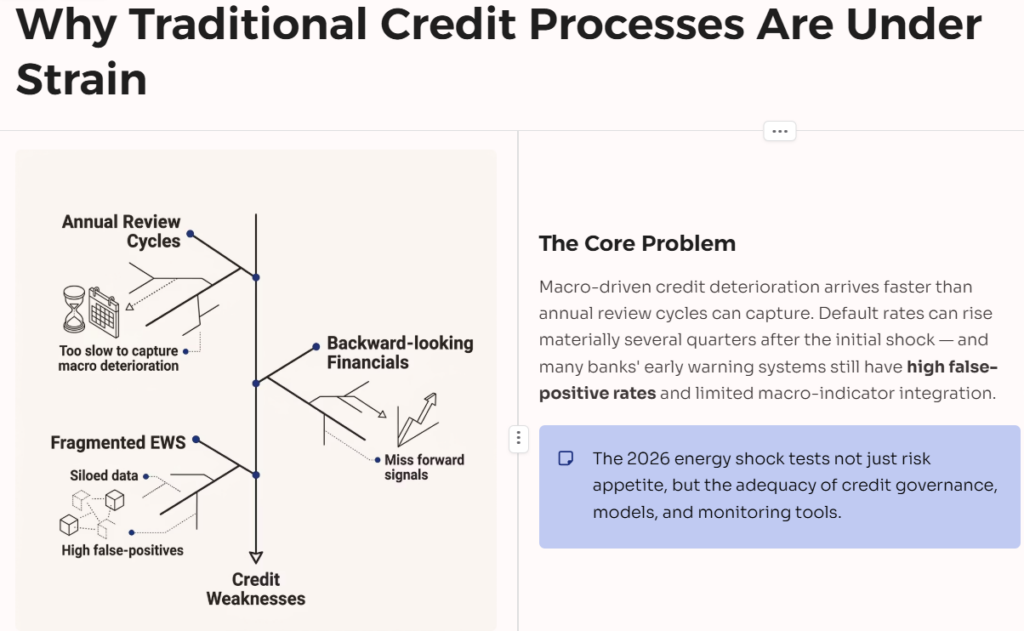

Why traditional credit processes are under strain

Academic and policy research on early‑warning indicators emphasizes that macro‑driven credit deterioration often arrives faster than traditional annual review cycles and rating processes can capture, especially when relying heavily on backward‑looking financials. Studies of NPL dynamics under macro shocks indicate that default rates can rise materially several quarters after the initial shock, with system‑wide effects depending on how quickly banks adjust underwriting, monitoring, and capital buffers.

At the same time, industry studies highlight challenges with early warning frameworks: many banks’ EWS still have high false‑positive rates, limited integration of macro indicators, and fragmented data infrastructure, reducing their usefulness in fast‑moving environments. The 2026 energy shock thus tests not just risk appetite but also the adequacy of credit governance, models, and monitoring tools.

Why This Matters from a Regulatory Perspective

Regulatory expectations increasingly emphasize forward-looking risk identification and portfolio segmentation:

- Industry-Level Monitoring: Aligning portfolios to OCC/SNC industry group classifications allows for more targeted risk identification

- Early Risk Rating Accuracy: Ensuring ratings reflect emerging stress before financial deterioration becomes evident

- Criticized Asset Migration: Energy shocks can accelerate movement into Special Mention and Substandard categories

- Defensibility: Examiners expect a clear linkage between macro developments and portfolio-level risk assessment

Institutions that proactively incorporate these dynamics into credit processes are better positioned in both risk management and regulatory dialogue.

How SRA Consulting Helps Banks Stay Ahead of the Cycle

In environments like this, the challenge is not identifying risk broadly—it is pinpointing where it will emerge first and acting before deterioration becomes visible.

SRA supports institutions by:

- Targeted Portfolio Segmentation: Identifying the 10–20% of exposures most sensitive to energy-driven stress

- Bottom-Up Stress Testing: Translating macro shocks into borrower-level impact on EBITDA, DSCR, and liquidity

- Independent Credit Review: Validating risk ratings and identifying emerging issues not yet reflected in internal assessments

- Early Warning Frameworks: Enhancing monitoring with forward-looking indicators tied to sector-specific risks

The goal is simple: move from reactive identification of problem loans to proactive risk management at the portfolio level.

How SRA Consulting’s credit services align with the current environment

Credit leadership and advisory: stabilising governance and policy

SRA’s Fractional CO Services provide interim credit leadership, policy refresh, and staff coaching, which are especially relevant where banks are rethinking sector appetites, underwriting standards, and workout strategies in light of elevated energy and interest‑rate risk. In the current environment, key leadership tasks include clarifying risk appetite for exposed sectors, tightening structures (covenants, amortisation, collateral), and ensuring exam‑ready documentation for CRE, C&I, and ABL portfolios.

SRA’s experience in improving CRE/C&I/ABL risk management and borrower‑touchpoint mapping can help institutions embed energy‑shock scenarios into policy, from property‑type DSCR floors to sector‑specific underwriting grids for transportation, materials, and consumer services.

Independent credit review and evaluation: objective diagnostics

Independent credit review, M&A due diligence, risk‑rating model validation, and CECL/allowance methodology services provide an external view of portfolio resilience and model adequacy.

- Independent Credit Review can focus on high‑risk books such as office, hospitality, and small‑business lending, sampling files to assess underwriting discipline, covenant enforcement, and early‑warning practice before regulators do.

- M&A Due Diligence is pertinent where institutions are acquiring portfolios with concentrated CRE or specialty‑finance exposure; rigorous credit marks and scenario‑based loss estimates help avoid overpaying for loans under energy‑stress conditions.

- Risk Rating Model Validation and CECL & Allowance Methodology support recalibration of PD, LGD, and Q‑factor overlays so that models capture the interaction of higher energy costs, inflation, and rates with borrower performance, consistent with emerging research on macro‑shock‑driven credit risk.

Portfolio risk analytics and capital planning: turning data into action

SRA’s Stress Testing, Early Warning Systems, Risk‑Based Capital Allocation, and Competitive Benchmarking services map closely to best practice recommendations from regulators and advisory firms.

- Stress Testing: Borrower‑level and top‑down macro stress tests can be tailored to the current shock, incorporating scenarios in which oil and gas prices remain elevated for multiple years, rates stay higher for longer, and growth moderates—a combination that research indicates would increase NPLs and pressure ROE.

- Early Warning Systems: Drawing on lessons from recent studies, SRA can help design or enhance EWS that use granular loan and behavioural data plus macro indicators (energy prices, inflation measures, sectoral indices) to identify distress several months before default, reducing false positives while improving “time before default.”

- Risk‑Based Capital Allocation: By linking sector‑ and rating‑level risk costs to capital, SRA can support capital frameworks that recognise the higher tail risk in energy‑sensitive sectors and the relative resilience of others, improving portfolio‑level ROE in line with scenario analysis.

- Competitive Benchmarking: Benchmarking against peers on NPLs, charge‑offs, sector concentrations, and allowance coverage helps boards and executives understand where their positioning is aggressive or conservative in the context of the energy shock.

Credit operations and monitoring: building scalable control frameworks

The current environment increases the operational burden on credit teams: exceptions multiply, manual tracking struggles to keep up, and regulators focus on the completeness and timeliness of monitoring. SRA’s Credit Portfolio Management, Exception‑Based Monitoring, Credit Process Modernization, and Problem Loan Management services address these pain points.[19][9]

- Credit Portfolio Management solutions provide scalable tools and routines for oversight and underwriting, supporting risk‑tiered review cadences and focusing scarce expert time on the highest‑risk names.

- Exception‑Based Monitoring can be used to automate tracking of covenant breaches, reporting delays, policy exceptions, and emerging arrears across CRE, C&I, and specialty‑finance portfolios, improving the bank’s ability to escalate and remediate issues before exams.

- Credit Process Modernization aligns credit workflows, documentation, and decisioning tools with updated risk policies, reducing friction and ensuring that heightened energy and interest‑rate considerations are systematically embedded from origination through monitoring.

- Problem Loan Management supports workout strategies, restructuring plans, and playbooks tailored to energy‑affected sectors, drawing on lessons from past downturns and current market conditions.

Underwriting, EV, and transaction advisory: navigating complex borrowers

Lending to leveraged or intangible‑asset‑heavy borrowers is particularly sensitive to higher discount rates and volatility. SRA’s Contract Underwriting and Enterprise Valuation & Leveraged Lending Advisory are therefore highly relevant.

- Contract Underwriting can relieve backlog and add specialist expertise for complex CRE, C&I, and SBA credits in vulnerable sectors, improving consistency and speed while integrating updated sector‑specific credit signals.

- Enterprise Valuation & Leveraged Lending Advisory supports EV modelling, policy design, and deep dives on leveraged borrowers; this is critical when energy and rate shocks compress EBITDA multiples and raise refinancing risk across sponsor‑backed and private borrowers.

Innovation, AI, and strategic foresight: future‑proofing credit risk

Rapid changes in macro conditions and data availability make innovation and responsible AI particularly valuable.

- Risk Innovation & Responsible AI Integration helps institutions explore AI‑powered underwriting, analytics, and review processes while maintaining ethical and regulatory compliance—an approach aligned with supervisors’ emphasis on explainable, forward‑looking risk tools and early‑warning capabilities.

- Environmental Risk and Regulatory Disclosure Advisory is pertinent as regulators and investors increasingly ask banks to articulate how climate and energy‑transition risks intersect with traditional credit risk and how they are reflected in stress tests, risk appetite, and disclosures.